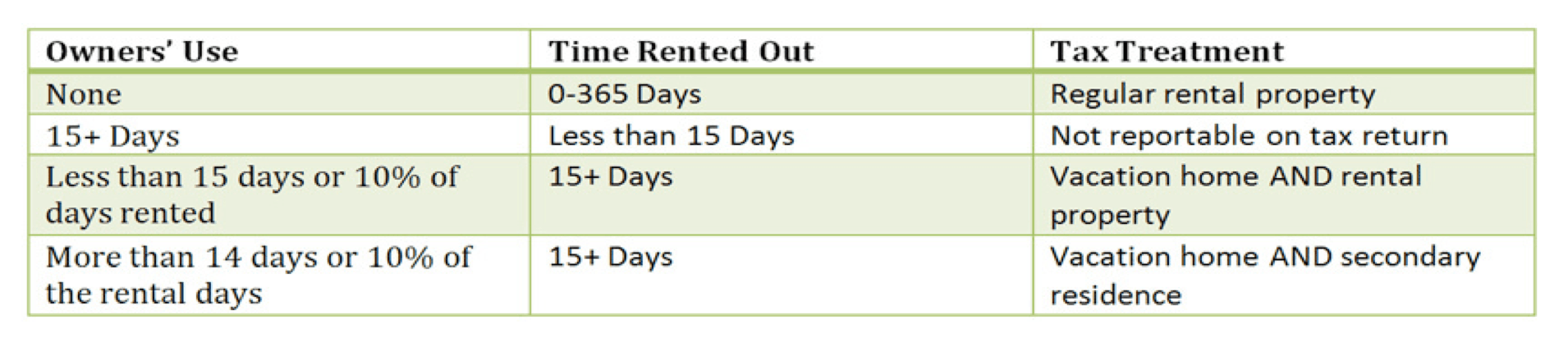

Permitted Expenses For Rental Income Malaysia : Solved 7 Norman And Sarah Who Are Married Are Both Mala Chegg Com : Permitted expenses incurred by an ihc consist of:

Permitted Expenses For Rental Income Malaysia : Solved 7 Norman And Sarah Who Are Married Are Both Mala Chegg Com : Permitted expenses incurred by an ihc consist of:. Thus, in appendix 1,the loan interest of rm35,000, although far in excess of the rental income of rm14,000 from the agricultural land, is fullyabsorbed against the grouped rental income. (a) 55/2019] please refer to the picture below for a sample on how to calculate rental income tax exemption. Expenses fulfilling the deductibility tests under s.33(1) are deductible from gross income in arriving at adjusted income.hence the loan interest, quit rent and assessment rates are deductible from the grouped rental income. Examples of such expenses include: General requirements for documenting rental income.

For simplicity, just remember that rental is in its own category and has its own progressive tax rate that ranges between 0 and 28%. Permitted expenses—such as repairs— are things that you need to spend on, like in the example we showed above. Furniture and fittings, electrical appliances and equipment, instead of claiming them as a deduction on a replacement basis; Deductible expenses in malaysia, rental income that you received from your real property such as serviced apartment, condominium, flat, shophouses, industrial properties, commercial office, etc is taxable under the income tax act 1967. Expenses which are allowed deduction from rental income are the direct expenses that are wholly and exclusively incurred in the production of the rental income.

Computation Of Buss Income Studocu from d20ohkaloyme4g.cloudfront.net Furniture and fittings, electrical appliances and equipment, instead of claiming them as a deduction on a replacement basis; A is the total of the permitted expenses incurred for that basis period reduced by any receipt of a similar kind; R 48 216 x 250 / 365 = r 33 024. (a) 55/2019] please refer to the picture below for a sample on how to calculate rental income tax exemption. (5% x 115,000) = 5,750, whichever is lower. For more comprehensive information, you can refer to lhdn malaysia public ruling no. 19 december 2018 from the letting of the real property is charged to tax as rental income under paragraph 4(d) of the ita. Deductible expenses in malaysia, rental income that you received from your real property such as serviced apartment, condominium, flat, shophouses, industrial properties, commercial office, etc is taxable under the income tax act 1967.

And c is the aggregate of the gross income consisting of dividend (whether exempt or not), interest and rent, and

Special personal income tax relief for year of assessment 2020 to resident individuals of up to rm1,000 for domestic travelling expenses incurred between 1 march 2020 to 31 august 2020. As well as rent, this includes any sum paid for the use of premises, such as service charges and car parking fees. Assessment even though income from the holding of investment is not less than 80% of the gross income of the company. Transfer pricing methodologies for transfer pricing 2012. This article first appeared in. Furniture and fittings, electrical appliances and equipment, instead of claiming them as a deduction on a replacement basis; For simplicity, just remember that rental is in its own category and has its own progressive tax rate that ranges between 0 and 28%. Income tax (exemption) (no.2) order 2019 p.u. Thus, in appendix 1,the loan interest of rm35,000, although far in excess of the rental income of rm14,000 from the agricultural land, is fullyabsorbed against the grouped rental income. Examples of such expenses include: a x b = 49,000 x 115,000 = 6,552 4c 4 x 215,000 compared with 5% of dividend, interest and rental income. However, when the rental is received in advance, the advance rental would be taxed in the year of receipt. Only franked dividends, permitted expenses will not be allowed.

However, when the rental is received in advance, the advance rental would be taxed in the year of receipt. Some of these permitted expenses include the cost of ordinary repairs to maintain the property in its existing state, insurance premium on fire/burglary, assessment tax and quit rent, as well as mortgage interest on loan obtained. The tenants are entitled to use the swimming pool, tennis court and other facilities B is the gross income consisting of dividend, interest and rent chargeable to tax for that basis period; Rental income (business) decreases in the year of assessment

Rental Income Exempted From Income Tax Malaysia And Other Tax Reliefs For Ya 2021 Propertyguru Malaysia from cdn-cms.pgimgs.com For simplicity, just remember that rental is in its own category and has its own progressive tax rate that ranges between 0 and 28%. Business income treatment is granted automatically by law (section 63c of the act). The amount of permitted expenses determined in accordance with the formula is: In malaysia, income derived from letting of real properties is taxable under paragraph 4 (a) (business income) or 4 (d) (rental income) of the income tax act 1967. You can deduct income generating expenses from the percentage of amount you will be taxed. Unless the renewal of tenancy agreement legally that done and charged by lawyer which could able to deduct direct expenses against the gross rental income. Income tax (exemption) (no.2) order 2019 p.u. A is the total of the permitted expenses incurred for that basis period reduced by any receipt of a similar kind;

A is the total of the permitted expenses incurred for that basis period reduced by any receipt of a similar kind;

The amount of permitted expenses determined in accordance with the formula is: If a borrower has a history of renting the subject or another property, generally the rental income will be reported on irs form 1040, schedule e of the borrower's personal tax returns or on rental real estate income and expenses of a partnership or an s corporation form (irs form 8825) of a business tax return. Only franked dividends, permitted expenses will not be allowed. Deductible expenses in malaysia, rental income that you received from your real property such as serviced apartment, condominium, flat, shophouses, industrial properties, commercial office, etc is taxable under the income tax act 1967. Interest, dividend, rental (non business and business of holding of an investment) is treated as a business source under section 4(a) of the act. B is the gross income consisting of dividend, interest and rent chargeable to tax for that basis period; Furniture and fittings, electrical appliances and equipment, instead of claiming them as a deduction on a replacement basis; Transfer pricing methodologies for transfer pricing 2012. Other instances of permitted expenses would be insurance and quit rent/maintenance. Example 7 azrie owns 2 units of apartment and lets out those units to 2 tenants. In malaysia, income derived from letting of real properties is taxable under paragraph 4 (a) (business income) or 4 (d) (rental income) of the income tax act 1967. General requirements for documenting rental income. You can deduct income generating expenses from the percentage of amount you will be taxed.

Much like personal income tax, corporate income tax is applied on a company's chargeable income after applying tax deductions. 19 december 2018 from the letting of the real property is charged to tax as rental income under paragraph 4(d) of the ita. Only franked dividends, permitted expenses will not be allowed. For more comprehensive information, you can refer to lhdn malaysia public ruling no. Example 5 income of mega central sdn bhd for the years of assessment 2010 to 2014 are as follows.

How To Report Rental Income On Foreign Property A Guide For Expats from www.greenbacktaxservices.com You are allowed to claim capital allowances on the capital expenditure employed to generate the rental income from your properties, eg. R 48 216 x 250 / 365 = r 33 024. Thus, in appendix 1,the loan interest of rm35,000, although far in excess of the rental income of rm14,000 from the agricultural land, is fullyabsorbed against the grouped rental income. For more comprehensive information, you can refer to lhdn malaysia public ruling no. Thus, only the interest portion of his loan repayment is recognised as deductible expenses which can be offset from his rental income. Deductible expenses in malaysia, rental income that you received from your real property such as serviced apartment, condominium, flat, shophouses, industrial properties, commercial office, etc is taxable under the income tax act 1967. Some examples of general permitted expenses for rental income are the cost of repair and maintenance (including repainting), security charges, fire or burglary insurance, agent fees incurred for. Tax deductions are business expenses incurred by the company for the sole purpose of gross income generation, and are deductible expenses allowed under provisions of the income tax act 1967.

The expenses wholly and exclusively incurred in the production of the rental income are allowable as a deduction to arrive at a net rental income.

Transfer pricing methodologies for transfer pricing 2012. Expenses which are allowed deduction from rental income are the direct expenses that are wholly and exclusively incurred in the production of the rental income. Inland revenue board of malaysia date of publication: Examples of such expenses are as follows assessment and quit rent, interest on loan and fire insurance premium, expenses on rent collection, expenses on rent renewal, expenses. Other instances of permitted expenses would be insurance and quit rent/maintenance. In simpler words, it's this equation: Example 7 azrie owns 2 units of apartment and lets out those units to 2 tenants. Much like personal income tax, corporate income tax is applied on a company's chargeable income after applying tax deductions. If a borrower has a history of renting the subject or another property, generally the rental income will be reported on irs form 1040, schedule e of the borrower's personal tax returns or on rental real estate income and expenses of a partnership or an s corporation form (irs form 8825) of a business tax return. In malaysia, income derived from letting of real properties is taxable under paragraph 4 (a) (business income) or 4 (d) (rental income) of the income tax act 1967. Expenses fulfilling the deductibility tests under s.33(1) are deductible from gross income in arriving at adjusted income.hence the loan interest, quit rent and assessment rates are deductible from the grouped rental income. The amount of permitted expenses determined in accordance with the formula is: Example 5 income of mega central sdn bhd for the years of assessment 2010 to 2014 are as follows.

Related : Permitted Expenses For Rental Income Malaysia : Solved 7 Norman And Sarah Who Are Married Are Both Mala Chegg Com : Permitted expenses incurred by an ihc consist of:.